The enabling environment for biodiversity credit markets: demand drivers, policies, and organizations leading the charge

Welcome back to part three of our series on biodiversity and nature markets.

We introduced this series by defining biodiversity and differentiating credits from offsets. For a quick recap, head over to our first post. Moving forward, we explored the biodiversity market, defining key industry players — see more on this in our second post. In this piece, we’ll take a look at buyer personas and demand drivers, as well as the enabling environment for voluntary market growth fostered by national and regional policies, intergovernmental initiatives, and cross-sectoral collaborations.

Corporate buyer personas: Who (and what) is driving demand for voluntary biodiversity credits?

One of the most common questions we encounter around biodiversity credits is: Why would a company buy voluntary biodiversity credits if they cannot be used to offset an entity’s nature footprint or comply with jurisdictional regulation? To understand the characters in this nascent voluntary market and their motivations, we can first look to corporate buyers in carbon markets. Although voluntary carbon credits are a unique asset class that is measured, and therefore valued and priced, differently from biodiversity credits, the voluntary nature of the market provides insight into how companies may interpret the threats and opportunities that accompany biodiversity assets.

Giulia M. Stellari, a member of the EU Expert Group on Carbon Removals and former Director of Sustainable Sourcing at Unilever, offers a helpful outline of three corporate carbon buyer archetypes:

The Risk Buyer — This company anticipates future regulatory developments that will require adjustments to core operations and/or raise costs. This company purchases voluntary credits to get ahead of the curve and develop an internal capacity for climate and nature related assessments, accounting, and compensation to ease the costs of transition when they are later regulated to do so.

The Trust & Leadership Buyer — This company is driven by a desire to label their products or services as climate or nature friendly in order to maintain trust between their brand and consumers. This company is most likely to be a first mover in the space, as they seek to source credits today and into the future that will enable continuous delivery on their planet positive claims.

The R&D Buyer — This company tracks market movement now in order to develop a line of business around advising and supplying others in the future. This persona includes professional and financial service firms, consultancies, and other intermediary actors who will help onboard new buyers into the market.

It is worth noting that none of these personas or motivating factors are cut and dry — demand is an intricate and overlapping force, especially with regard to a topic as complex as nature and biodiversity.

Now that we have an understanding of some buyer personas, let’s look deeper into the forces motivating their behavior in biodiversity and nature markets. A December 2023 report from the World Economic Forum (WEF) presents six key demand drivers for biodiversity credits that track closely onto these buyer personas. The report makes a distinction between internal drivers, where a business benefits directly from biodiversity improvement, and external drivers, which consider the expectations and opinions of stakeholders outside of the company.

A WEF working group chaired by McKinsey & Co. identified six key demand drivers for voluntary biodiversity credits. Source: WEF (2023).

Internal drivers include:

Mission — Corporates see a need to elevate nature’s importance alongside carbon in organizational objectives, as leadership recognizes the significance of aligning company values to attract and retain employees. Candidates in the workforce today are increasingly factoring company ethics, sustainability, and mission into their career choices. A 2022 IBM study found that 68% of participants were more likely to accept jobs from environmentally driven organizations over organizations that do not have this mission alignment.

Ecosystem services and business dependencies — Companies acknowledge the vital role of unpriced ecosystem services (e.g. pollination and ecosystem regulating forces like clean water and air) that are supported by biodiversity. Downstream sectors, like retail, are now inclined to invest in biodiversity to safeguard access to natural assets and minimize the risks of business disruptions or raw material price shocks.

External drivers include:

Market differentiation — Companies demonstrating effective stewardship of biodiversity and nature are appealing to a growing segment of consumers who actively seek planet positive labels on products and are willing to pay extra for positive environmental outcomes.

Reputation — As civil society, financial institutions, and consumers increasingly demand transparent disclosure of environmental impacts and efforts to address nature loss, demonstrating good environmental performance becomes a greater priority for businesses across various sectors.

Regulation — Companies will seek to stay ahead of regulations, especially across Europe where the EU and individual member states are taking action on nature related impacts of consumer goods industries and land development (more on this below). The shift toward mandatory disclosure standards is prompting increased scrutiny of impacts both within and beyond company operations and supply chains.

Finance — Investors and financial lenders are demonstrating increasing demand for nature-friendly portfolios. For companies, this means a positive biodiversity track record or ESG rating can increase a company’s appeal to investors and lenders, reducing reputational and regulatory risks and subsequently lowering the cost of capital.

A closer look at regulation: National and regional policies moving supply and demand

Although voluntary biodiversity credit markets are not directly regulated by jurisdictional authorities, national and regional policies and the ways in which they shape compliance markets provide important signals for actors operating in the voluntary market.

Here are some of the earliest movers in nature and biodiversity regulation at the national and regional levels:

Germany’s Compensation Area Management law enacted in 2010 is designed to protect the value of nature and landscapes to safeguard biological diversity, the efficiency and functionality of natural balance, and its recreational value.

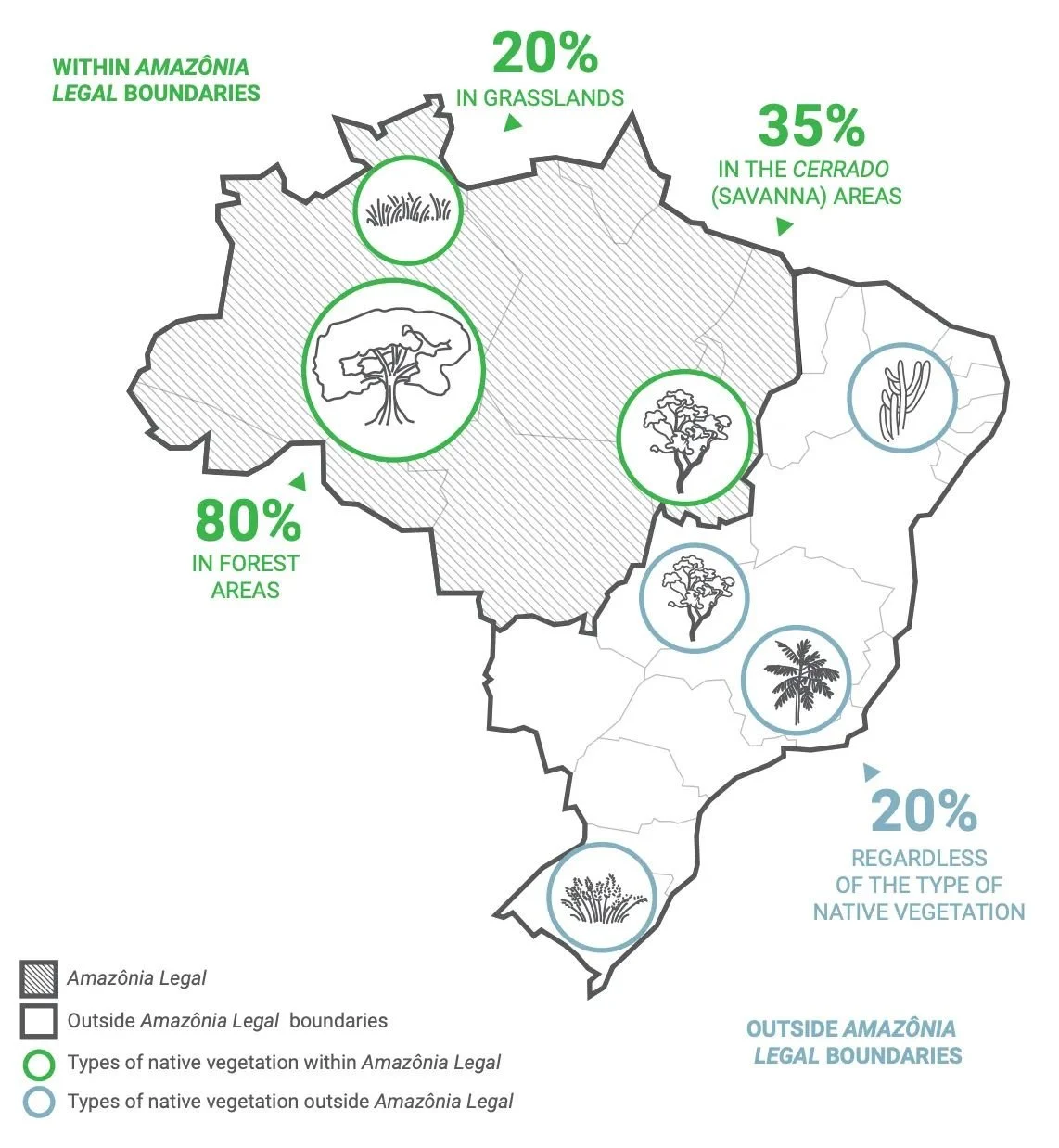

In Brazil, rural property owners are required to maintain native vegetation on 20%-80% of their land (depending on the type of vegetation present), known as “Legal Reserves” (LR). These LRs are intended to preserve ecosystems and ensure ecological balance. The latest revisions to Brazil’s Forest Code (originally passed in 1934, but revised in 1965 and 2012) established the Cotas de Reserva Ambiental (CRA) program, aiming to create a market where landowners with LR deficits can meet their legal obligations by purchasing “environmental reserve quotas”.

In 2015, South Africa introduced section 37D into the Income Tax Act offering a deduction for the value of land declared under the National Environmental Management: Protected Areas Act. This serves as a revenue stream for national biodiversity stewardship and conservation efforts.

Luxemburg introduced a biodiversity offset and ecopoints scheme in 2018 to compensate for ecological damage caused by private and public buildings.

Article 29 of France’s Law on Energy and Climate, which took effect in 2023, requires financial institutions to disclose biodiversity related risks.

The EU Regulation on Deforestation-Free Products, which entered into force in June 2023, has widespread impacts on consumer goods, retail, food and beverage companies.

In July 2023, the EU Nature Restoration Law was passed requiring member states to create national plans to restore nature within the EU’s land and sea boundaries. It includes specific, legally binding targets for the restoration of particular habitats and species, and is set to encompass a minimum of 20% of the EU’s land and sea areas by 2030, with the ultimate goal of restoring all ecosystems in need of rehabilitation by 2050.

The UK’s Biodiversity Net Gain (BNG) policy, which takes effect in 2024, mandates a 10% gain in biodiversity in areas that are permitted for land development (i.e. for the construction of hotels, community spaces, etc.) This policy mainly affects land developers, construction companies, and local planning authorities, and is a call to action for markets that revolve around housing, industrial, and commercial development. By 2030, the UK aims to generate £1 Billion of private investments for nature annually.

Brazil’s Forest Code mandates the preservation of 20%–80% of native vegetation per plot of land. Source: Climate Policy Initiative (Chiavari and Lopes, 2015).

While the most recent of these policy developments are taking place in Europe, Brazil and South Africa stand out for their early leadership in nature regulation across South America and Africa.

With national and regional regulations continuing to develop, there is reason to believe corporate demand for voluntary biodiversity credits will also continue to grow. In particular, businesses that identify as “Risk Buyers” will likely seek experience in voluntary biodiversity markets in the coming years to limit costs and disruptions to their operations that may be required for future compliance efforts.

Intergovernmental collaborations & the enabling environment for biodiversity credits

Alongside these national and regional bloc regulations, several noteworthy intergovernmental collaborations have emerged in the last three years, which are fostering an enabling environment for market growth:

In 2021, the UK and France launched a joint roadmap for mobilizing nature finance through biodiversity credits. This roadmap aims to expand the utilization of biodiversity-positive carbon credits and biodiversity certificates while structuring biodiversity credit markets for meaningful, equitable, and nature-positive results.

The 10 Point Plan: At the 77th UN General Assembly in September 2022, Ecuador, Gabon, the Maldives, and the UK launched a non-legally binding framework to address biodiversity loss by closing the global nature finance gap. The UK then went on to host an event in February 2023 called “Nature Action: Private Sector Mobilization” to shed light on the private sector’s role in transitioning to nature positive economies.

Positive Conservation Partnerships (PCP): At the One Forest Summit in Gabon in March 2023, France introduced the PCP with the goal of creating payment mechanisms, including biodiversity credits, backed by an initial €100 Million investment. At the summit, the Global Environment Facility (GEF) underscored the importance of scaling biodiversity certificates to address the funding shortfall for the preservation and restoration of nature, as well as ensuring the involvement of Indigenous Peoples and Local Communities (IPLCs) in shaping and benefiting from these certification initiatives.

New organizations driving cross-sectoral collaboration

The cultivation of this enabling environment at the intergovernmental level has been complemented by the formation of several key independent organizations to address nature markets. This is a promising sign of collaboration between the public and private sectors.

NatureFinance established the Task Force on Nature Markets in March 2022 to provide a practical governance framework for nature markets on the rise.

The Biodiversity Credit Alliance was established in December 2022 at the biodiversity COP15 in Montreal with support from the Swedish International Development Cooperation Agency (SIDA), the United Nations Development Programme (UNDP), and the United Nations Environment Programme Finance Initiative (UNEP-FI). Its purpose is to provide guidance for both project developers and buyers in building a credible and scalable market for voluntary biodiversity credits.

In September 2023, the Taskforce on Nature-Related Financial Disclosures (TNFD) published its final recommendations to facilitate the integration of nature impacts into decision-making, risk management, and disclosures to reach nature-positive outcomes.

In early 2024, the WEF is gearing up to introduce a Biodiversity Credit Buyers Club to boost corporate engagement and advanced market commitments.

Through the Finance for Biodiversity Pledge, 150 financial institutions are seeking to evaluate their biodiversity impact, establishing targets, and reporting on biodiversity metrics matters by 2024. Motivated by client preferences for nature-positive exposure, these institutions may strategically integrate biodiversity credits into their portfolios.

Nature Action 100 is the first global investor engagement initiative set to catalyze corporate ambition and action to reverse nature and biodiversity loss. It calls on companies to take timely and necessary actions to protect and restore nature.

Whether motivated by risk, reputation, or market advantage, momentum is building across the public and private sectors for voluntary biodiversity credits and nature markets. With new policies taking effect and buyers clubs coming on the scene throughout 2024, we’ll be collaborating with leading entrepreneurs and industry experts this year to share more market updates, tech developments, and policy news on climate and nature action. Follow Climate Collective on Medium and LinkedIn so you don’t miss a beat.